On October 17, 2017, the Office of the Superintendent of Financial Institutions (OSFI) issued a revision to mortgage qualification guidelines in Canada. The changes will go into effect on January 1, 2018, and will require conventional mortgage applicants to qualify at the Bank of Canada’s five-year benchmark rate or the customer’s mortgage interest rate plus 2%, whichever is greater.

OSFI’s Mortgage Stress Test

OSFI is implementing these changes for all federally regulated financial institutions. As a result, some customers looking to purchase a home or refinance may experience a reduction in the total principal amount they are qualified to borrow. We estimate that the average Canadian family’s home purchasing power for a given income to be reduced by between 18 and 20%.

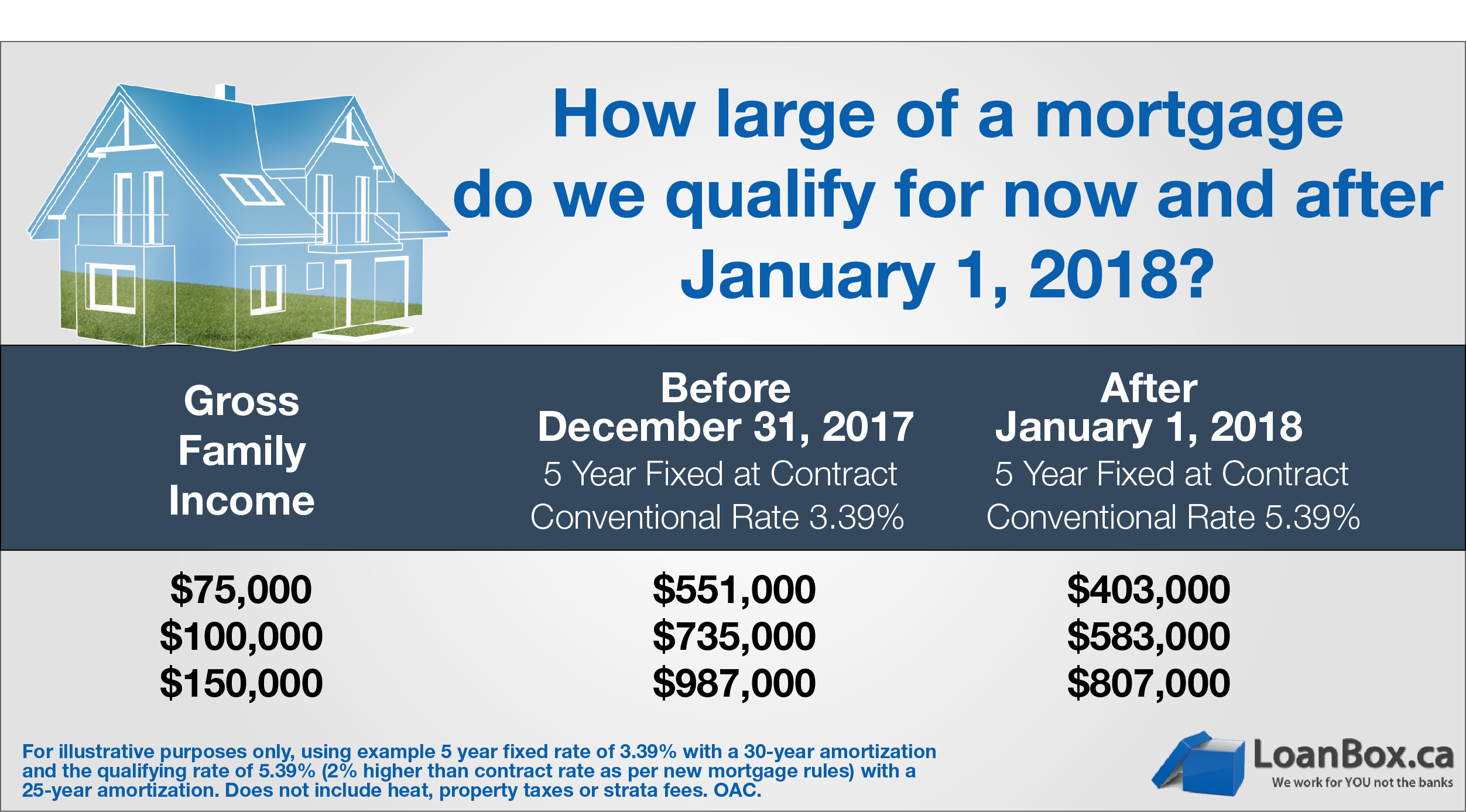

Here’s an example of the impact the new qualifying rate will have on the maximum mortgage loans based on a Canadian family income of $75,000, $100,000, and $150,000.

For illustrative purposes only, using example 5 year fixed rate of 3.39% with a 30-year amortization and the qualifying rate of 5.39% (2% higher than contract rate as per new mortgage rules) with a 25-year amortization. Does not include heat, property taxes or strata fees. OAC.